Introduction

One of the most important functions of an Islamic bank is the mobilization of deposits and investments from customers. Similar to conventional banks, Islamic banks provide facilities for safekeeping funds, making payments, saving money, and investing for future financial goals.

The key difference lies in the underlying Shariah principles. Rather than relying on interest-based arrangements, Islamic banks structure their products through Shariah-compliant contracts that promote fairness, transparency, and ethical financial practices.

This article provides an overview of the major deposit and investment products offered by Islamic banks and explains how they operate within the framework of Islamic finance.

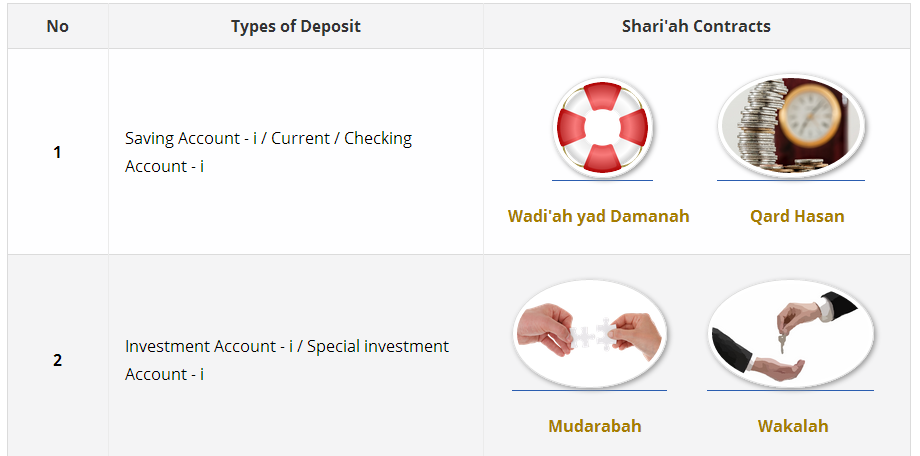

- Current Accounts

- Savings Accounts

- Term Deposit Accounts

- Investment Accounts

DEPOSIT PRODUCTS IN ISLAMIC BANKING: DEPOSIT ACCOUNTS

Current Account Operations

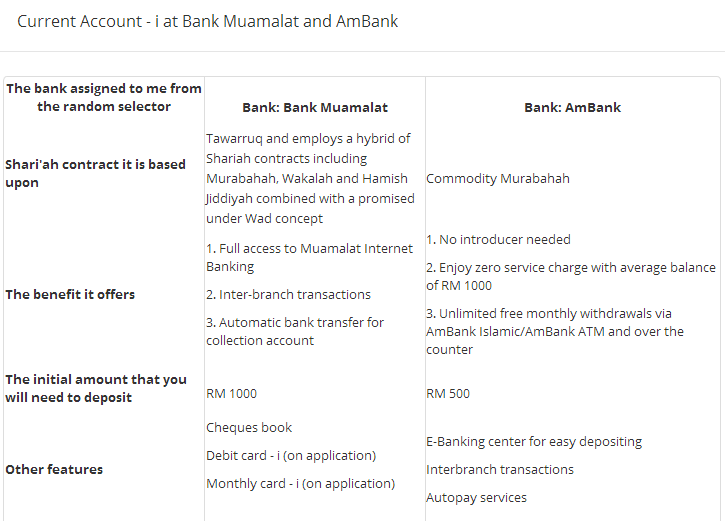

Current Account-i

Current Account-i

Purpose

A Current Account-i is designed for customers who require convenient and frequent access to their funds for daily transactions.

These accounts are commonly used by:

- Individuals

- Businesses

- Government agencies

- Associations and organizations

Customers can make payments, receive transfers, issue cheques, and manage cash flows efficiently.

Key Features

A Current Account-i typically offers:

- Cheque facilities

- Online banking services

- Fund transfers

- Standing instructions

- Auto-debit arrangements

- Trade and collection services

An initial deposit is usually required when opening the account.

Shariah Principle

Current accounts commonly operate under:

Wadiah Yad Dhamanah

(Guaranteed Safekeeping)

Under this arrangement:

- The customer deposits money with the bank.

- The bank guarantees repayment of the deposited funds.

- The bank may utilize the funds for its operations.

- Any hibah (gift) granted to the customer is entirely at the bank's discretion.

Some Islamic banks may also structure current accounts using Qard Hasan (benevolent loan) concepts depending on regulatory framework.

Savings Account-i

Purpose

A Savings Account-i is intended for customers who wish to save money while maintaining easy access to their funds.

Customers can withdraw money whenever needed through:

- ATM cards

- Debit cards

- Mobile banking

- Online banking.

Key Features

Savings accounts generally provide:

- Flexible deposits

- Flexible withdrawals

- ATM access

- Online banking access

- Account statements or passbooks

Unlike current accounts, savings accounts do not normally include cheque-writing

Shariah Principle

Savings accounts are commonly structured using:

Wadiah Yad Dhamanah

or

Qard Hasan

Under these structures:

- Depositors' funds are protected.

- Banks may voluntarily provide hibah.

- Hibah is not guaranteed and remains entirely discretionary.

This distinction is important because predetermined returns would resemble interest, which is prohibited under shariah.

Hibah in Islamic Banking

What is Hibah?

Hibah means a gift voluntarily given by the bank to its customers.

Unlike interest:

- It is not promised.

- It is not contractually guaranteed.

- It depends entirely on the bank's discretion.

Many Islamic banks provide hibah to reward customer loyalty while maintaining Shariah compliance.

Current Account-i versus Savings Account-i

Although both accounts provide safe custody of funds, there are important differences.

Current Account-i

Designed primarily for:

- Businesses

- Frequent transactions

- Cheque issuance

- Cash management

Savings Account-i

Designed primarily for:

- Personal savings

- Day-to-day financial needs

- ATM and online access

- Building financial reserves

The choice depends largely on customer objectives and transaction requirements.

Term Deposit Accounts

Commodity Murabahah Deposit (CMD)

Term deposits in Islamic banking are commonly structured using Commodity Murabahah or Tawarruq arrangements.

This product provides customers with:

- Capital preservation

- Predetermined profit rates

- Fixed investment

How Commodity Murabahah Works

The process generally involves:

- Customer purchases Shariah-compliant commodities.

- Customer sells the commodities to the bank at a deferred price.

- The deferred sale price includes an agreed profit margin.

- The bank settles payment upon maturity.

Because the transaction is based on trade rather than lending, it complies with Shariah requirements.

Benefits

Commodity Murabahah Deposits provide:

- Predictable returns

- Low risk

- Capital protection

- Fixed investment tenure

Investment periods may range from:

- 1 month

- 3 months

- 6 months

- 12 months

- Up to several years.

Investment Accounts

Purpose

Investment Accounts are designed for customers who wish to participate in Shariah-compliant investments and potentially earn higher returns.

Unlike deposit accounts:

- Returns are not guaranteed.

- Investors share risks and rewards.

- Performance depends on actual investment

Types of Investment Accounts

Unrestricted Investment Account (URIA)

Under an Unrestricted Investment Account:

- Customers provide funds.

- The Islamic bank determines investment opportunities.

- The bank manages the investment according to its expertise.

The customer does not specify where funds must be invested.

Restricted Investment Account (RIA)

Under a Restricted Investment Account:

- Customers specify investment requirements.

- The bank must follow the investor's mandate.

Examples include:

- Real estate projects

- Infrastructure projects

- Specific industries

- Particular investment portfolios

This provides greater control to investors.

Mudarabah Investment Accounts

One of the most common structures for investment accounts is Mudarabah.

Parties Involved

Rabb-ul-Mal

The investor who provides capital.

Mudarib

The Islamic bank acting as fund managers.

Profit and Loss Sharing

If investments generate profits:

- Profits are shared according to a predetermined ratio.

If losses occur:

- Investors bear financial losses.

- The bank loses its effort and management fees.

However, if losses arise from negligence, misconduct, or breach of mandate by the bank, the bank may be held responsible

Wakalah Investment Accounts

Another popular structure is Wakalah.

Under Wakalah:

- Investors appoint the bank as an investment agent.

- The bank manages investments on behalf of investors.

- The bank earns an agreed management fee.

Investment returns belong primarily to investors after deducting applicable fees.

Special Investment Accounts

Special Investment Accounts

Special Investment Accounts are similar to Restricted Investment Accounts.

Funds are directed toward:

- Specific projects

- Specific industries

- Specific investment opportunities

Investors generally understand:

- Expected risks

- Investment objectives

- Profit-sharing arrangements

This makes them suitable for medium- and long-term investment strategis.

Practical Example

Suppose a company wishes to convert its conventional banking facilities into Islamic banking.

Its needs may include:

Transactional Funds

A Current Account-i provides liquidity and payment convenience.

Staff Salary Management

A Savings Account-i allows easy salary disbursement and withdrawals.

Short-Term Capital Preservation

A Commodity Murabahah Deposit offers fixed-term returns.

Growth-Oriented Investments

A Mudarabah or Wakalah Investment Account allows participation in Shariah-compliant investments.

Different financial needs require different Islamic banking products.

Conclusion

Islamic banking offers a comprehensive range of deposit and investment products that serve the same practical purposes as conventional banking while adhering to Shariah principles.

The main objectives are:

- Protection of wealth

- Fairness in transactions

- Transparency

- Ethical investment

- Risk sharing

Whether through Current Accounts, Savings Accounts, Commodity Murabahah Deposits, Mudarabah Investment Accounts, or Wakalah Investment Accounts, Islamic banking seeks to provide financial solutions that are both commercially viable and spiritually responsible.

Understanding these products helps customers make informed financial decisions while participating in a banking system that aligns with Islamic values and principles.

No comments:

Post a Comment